Tokenization is one of the biggest buzz words around, right after “Bitcoin halving” and “DePin”. As highlighted in my last post, the blockchain movement is in the midst of a much needed metamorphosis to enable widespread adoption. While scaling is being sorted (i.e. the “how” part of the equation), the “why” element is equally, if not more, important to figure out. Blockchain technology has long been criticized as a solution without a problem. So, what uses require blockchains to scale? I believe decentralized finance (DeFi) is a core use case for blockchain, and tokenization is one of its most valuable applications.

Status quo has no flow

Traditional finance has long been plagued with huge time and cost inefficiencies for businesses and individuals alike. Centralized infrastructure managed by centralized authorities and intermediaries have resulted in a lack of transparency, high transaction costs and high barriers to entry. At a higher level, building financial systems on open, permissionless blockchain networks removes the need for intermediaries while putting control into the hands of the user. Digging a little deeper, DeFi helps users send, receive, borrow and invest money without involving third-parties, using self-executable smart contracts. All transactions on blockchains are publicly verifiable ensuring transparency; at the same time, transactions are encrypted which also enables security. Moreover, as blockchain networks evolve, new applications and financial systems can be built on top of existing ones in a modular fashion, providing additional functionality and creating an interoperable or composable ecosystem. With traditional finance, most existing systems are disparate, with no way of integrating them. Given the number of intermediaries involved there is counterparty risk, which stems from the disparity of the systems involved. And these systems and applications are sticky; once businesses or individuals have been onboarded, it’s harder to try something new or move to a better service given the laborious process involved.

For instance, if you want to invest in an equity-based investment product, first, you need to transfer funds from your bank to a trading/investment platform (this can take 1-3 business days and often incurs a fee). Assuming you already have an investment account setup, you can place a buy order and the order will be executed, either immediately (in the case of stocks, options and ETFs) or at the end of the business day (for mutual funds), also for a fee. Instead, DeFi allows you to operate 24/7 with no intermediaries in play and instantaneous settlement! You can store your cryptocurrency in a wallet such as MetaMask, which integrates with many investment applications such as Aave and Uniswap and invest seamlessly, with lower fees compared to traditional investments.

The “what”, “how” and “why”?

A core tenet of decentralized finance (DeFi) is real-world asset (RWA) tokenization. This is the process of transforming RWAs into digital tokens which are stored on blockchains. Personally, I like the definition in Chainlink’s blog; “… [a] digital representation of the underlying asset is created, enabling onchain management of the asset’s ownership rights and helping to bridge the gap between physical and digital assets.” RWA tokenization has altered how these assets can be accessed, exchanged, and managed, while offering enhanced liquidity, transparency, and less friction. These RWAs can range from the “core” traditional assets like cash, commodities, equities, and bonds, to alternative asset classes like real estate, artwork, intellectual property, and even luxury watches (here’s looking at you, Kettle Finance!).

How do RWAs get onchain? Once the RWA has been identified, smart contracts are created with clear rules on how tokens will be created, managed and traded. The next step is to pick the appropriate blockchain platform for the token. Some institutions select private blockchain networks (often due to regulatory concerns), while others select public blockchains such as Ethereum or Solana and consequently the appropriate token standard. A token standard is a set of rules and conditions the token follows; for instance, ERC-20 is a typical Ethereum-based standard for fungible tokens while ERC-721 is a blueprint for non–fungible tokens. Tokens are then distributed to investors through private sales, auctions, or public offerings, depending on the regulatory framework. Through the token lifecycle, the issuer is responsible for compliance and regulatory requirements as well as managing the underlying asset.

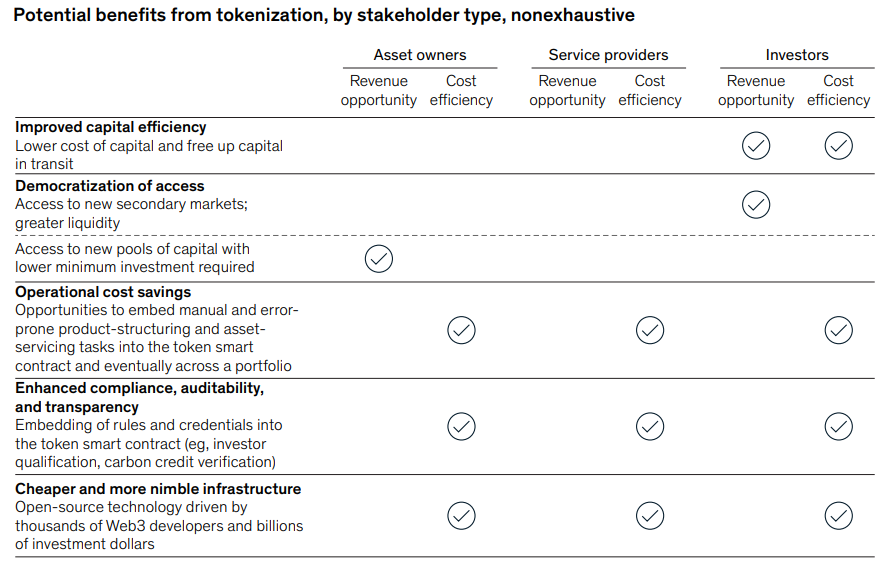

And the benefits are evident! Per a recent report by McKinsey, benefits of tokenization is illustrated in the table below, showing the cost efficiencies which yield improved revenue capture:

What’s out there?

There are many exciting tokenized offerings in the market today, appealing to all investment appetites on the risk-return spectrum. One of the most prolific TradFi names out there, BlackRock launched an Ethereum-based tokenized fund called BUIDL in March 2024, representing investments in U.S. treasuries and repurchase (repo) agreements, and had a market cap of ~$286 million just three weeks after being launched. Ondo Finance is paving the way for easy access to institutional-grade investments, with token offerings representing a highly liquid strategy including short-term U.S. treasuries, yield-generating USD-denominated stablecoin, and U.S. money market funds. On the blockchain native-side of the market are Aave and Uniswap, both of which are Ethereum-based. Uniswap is a leading decentralized exchange (DEX) where digital assets can be traded and liquidity pools are provided in a permissionless manner. Aave is a lending protocol, allowing users to lend and borrow cryptocurrencies through smart contracts, using liquidity pools to enable liquidity. In the “alternatives” world, RealT offers fractionalized ownership in U.S. real estate through tokens, while Parcl offers exposure to U.S. real estate markets by tokenizing synthetic digital assets.

Holdback to adoption

Even with a deep ecosystem in tokenized assets out there, adoption remains limited. The first asset tokenization occurred in 2017. So what is holding this space back?

Infrastructure readiness

- There is a shortage of custody and wallet solutions which are institutional-grade and catered to digital-assets offering flexibility in managing account policies, such as trading limits.

- Lack of uptime during high transaction throughputs is another constraint. This is being addressed through scaling measures across public blockchains (modular blockchains, sharding, and more recently the Dencun upgrade on Ethereum); however, there is no magic solution – take a look at the recent congestion issues on Solana!

- Additionally, the lack of interoperability for private blockchain tooling makes the space fragmented with higher systemic risks.

Nascent ecosystem

The ecosystem is not mature enough to leverage the instantaneous settlement advantages of tokenization. Cross-bank solutions are limited and stablecoins do not have regulatory clarity to be considered as a “bearer asset”.

Regulatory uncertainty

As McKinsey points out, “U.S. players are particularly challenged by undefined settlement finality, lack of legally binding status of smart contracts, and unclear requirements for qualified custodians.” The capital treatment of digital assets is also viewed more severely than traditional assets making it more costly to hold and distribute digital assets.

Where do we go from here?

While the infrastructure elements are being sorted through, the core challenges are centered around convincing regulators and institutions that tokenization and fundamentally blockchain technology is worth investing in. Push back from the SEC and legislators on Capitol Hill needs to be tackled systematically and collectively today. An overhaul of the financial system is no easy task. But the transparency, lower risk and cost efficiencies which stem from the adoption of tokenization can help fix the opaque and disparate financial systems we deal with on a day-to-day.